Picture supply: Getty Pictures

It’s all the time a bit surreal when an organization in your Shares and Shares ISA begins trending big-time internationally. That’s what occurred to me just lately with cybersecurity agency CrowdStrike (NASDAQ: CRWD).

That is the kind of firm that I need working behind the scenes, maintaining its clients secure from cyber threats with its cloud-native Falcon platform. If its title is out of the blue on everybody’s lips, then I’d assume an enormous cyberattack has taken place.

As we all know although, that’s not what occurred just a few days in the past. A defective software program replace crashed 8.5m Microsoft Home windows computer systems, disrupting flights, banks, TV channels, and hospitals around the globe. It was the largest IT outage in historical past.

Following this, the CrowdStrike share worth has dropped 23%. Is that this an opportunity for me to purchase extra shares?

A family title (for the mistaken cause)

The very first thing to notice is that there’ll clearly be significant claims from this epic failure. Delta Air Traces, for instance, has needed to cancel greater than 4,000 flights.

This occasion even triggered volatility among the many largest cyber underwriters throughout the first and reinsurance markets. Barclays mentioned: “At current, as a result of brief period of the accident and the non-malicious nature of it, we might anticipate [insurance] trade influence of $1bn or much less.”

As disruptive as this was, and positively embarrassing for CrowdStrike, a large-scale cyberattack would have been worse. That might have destroyed belief within the firm’s defensive capabilities.

Then once more, there’s nonetheless the unquantifiable reputational injury. That may take time to measure.

What we do know is that Elon Musk has mentioned that Tesla has already deleted CrowdStrike from its methods. Others might but comply with and that may clearly influence the corporate’s progress prospects.

An necessary platform

Stepping again although, the widespread influence of this occasion highlights how necessary the corporate’s endpoint safety platform has develop into. It now serves 538 of the Fortune 1000 firms, whereas its synthetic intelligence (AI) expertise will get smarter because it consumes extra knowledge.

Between FY19 and FY24 (which resulted in January), income grew by greater than 10 occasions.

In Q1 FY25, the corporate generated document free money stream of $322m, up from $227m a yr in the past. That was 35% of its $921m in income, which grew 33%.

It’s been rolling out extra AI options, with 28% of its clients adopting seven or extra of its 28 cloud modules, up from 23% a yr earlier.

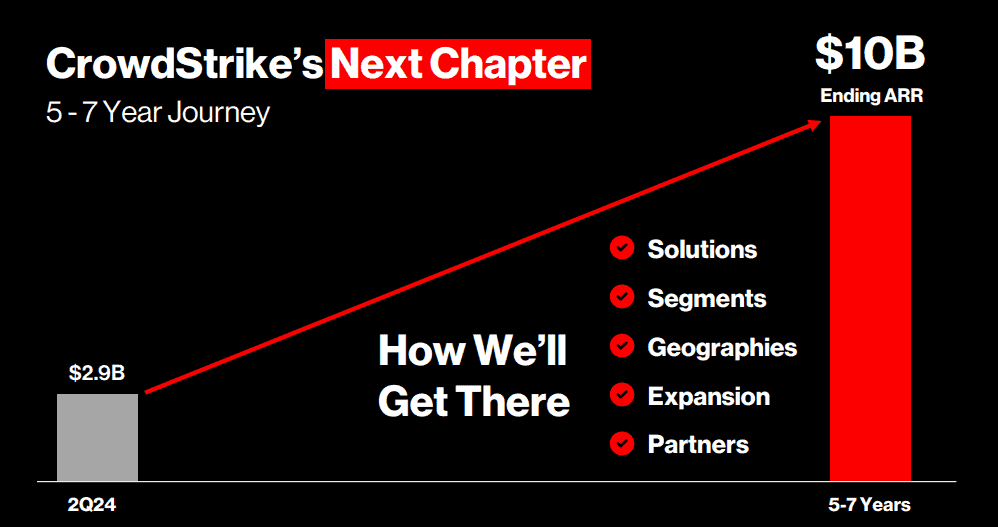

Wanting forward, the agency is concentrating on $10bn in annual recurring income (ARR) over the following 5 to seven years. On the finish of Q1, ARR stood at $3.65bn.

In fact, this goal was made earlier than the software program replace debacle.

My transfer

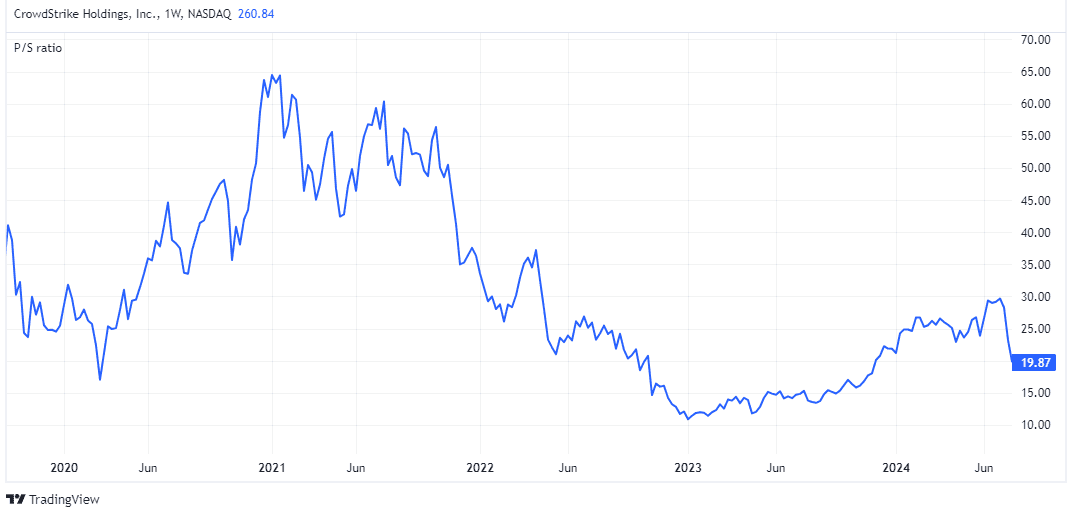

CrowdStrike is buying and selling at round 20 occasions gross sales, even after the 23% drop. So this stays a really costly inventory — one priced for perfection.

Nevertheless, issues aren’t excellent. Development charges may drop off if there are points with renewals and attracting new clients. In the meantime, the agency might have to supply some worth concessions or redesign how its software program interacts with units, placing stress on near-term profitability.

However, this stays a best-in-breed cybersecurity inventory. If it retains on falling, I’ll think about investing extra money. However I’d desire to attend for Q2 in August to listen to administration converse.