Picture supply: Getty photos

The Bunzl (LSE:BNZL) share value has risen by a whopping 88% over the previous decade. And whereas it’s down for the reason that begin of 2024, the corporate is staging a comeback as gross sales and margins present indicators of restoration.

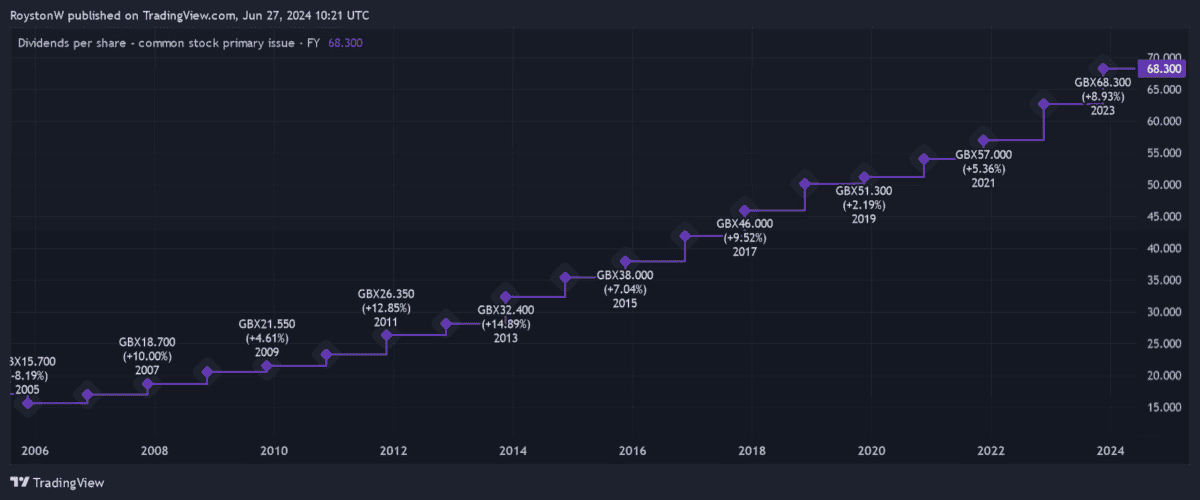

I’m on the lookout for the perfect passive revenue shares to purchase in July. And Bunzl — with its 31 straight years of dividend progress — is close to the highest of my procuring listing.

The truth is, following a wonderful buying and selling assertion as we speak (27 June), I’ll lastly be about to drag the set off. Right here’s why.

A steady performer

Help providers large Bunzl sells a variety of important merchandise to quite a lot of sectors throughout the globe. This contains meals packaging to supermarkets, disinfectant to cleansing companies, gloves to medical professionals, and onerous hards to development firms.

Put merely, its provision of on a regular basis items and providers helps the world go spherical. Because of this, earnings are usually steady in any respect factors of the financial cycle, which in flip offers Bunzl the energy and the boldness to ship that long-term dividend progress I discussed above.

Revenue improve

However the firm hasn’t had all of it its personal far more lately. Weak buying and selling in North America has impacted revenues and margins, and this stays a menace if rates of interest fail to meaningfully backtrack from present ranges.

Bunzl confirmed as we speak that gross sales are more likely to have dipped 3% to 4% within the first half, or 0% to 1% at steady currencies. It stated that “quantity reductions and deflation in our US enterprise” will seemingly drive revenues decrease.

Nonetheless, a pointy uptick in working margins helps to offset this drawback. Certainly, Bunzl stated margins are actually anticipated to beat 2023’s ranges, which in flip prompted the agency to boost its earnings forecasts for the complete 12 months.

It stated that efficient margin administration and the good thing about acquisitions imply that “good margin progress is anticipated in North America within the first half of the 12 months and really robust margin progress within the UK & Eire and Remainder of the World.”

Bunzl additionally stated it now expects to announce “strong income progress” at fixed currencies for the complete 12 months.

Dividend progress

| Yr | Dividend per share | Dividend progress | Dividend yield |

|---|---|---|---|

| 2023 | 68.3p | + 8.9% | 2.2% |

| 2024 | 72p (f) | + 5.4% | 2.3% |

| 2025 | 76p (f) | + 5.6% | 2.5% |

| 2026 | 79.3p (f) | + 4.3% | 2.6% |

So what dooes this replace imply for future dividends? Properly, Metropolis analysts have been anticipating payouts to proceed rising earlier than Thursday’s replace, as proven within the desk above. Right now’s information is bound to bolster their bullish estimates.

On the draw back, brokers assume dividends will develop at a extra modest fee than in earlier years. The payouts on Bunzl shares have risen at a compound fee of round 9% since 1992.

Nonetheless, dividend progress is anticipated to outpace that of the broader FTSE 100. As an illustration, AJ Bell tasks a modest 2.3% rise in money rewards (together with particular dividends) for 2024. That is lower than half the expansion fee brokers anticipate for Bunzl’s dividends this 12 months.

And if the enterprise can maintain its latest momentum going, analysts may truly improve their dividend forecasts for the short-to-medium time period. I believe dividend chasers ought to give Bunzl shares a detailed look proper now.